This Cyprus real estate market report takes a deep dive into the recent development of the Cypriot real estate sector and its development. Let the real estate specialists at Property Experts Cyprus take you on an exclusive tour across all districts of this Mediterranean island.

With our extensive market expertise and data analytics, we take a look at the residential housing market for apartments and houses, as well as a buyer profile and overall real estate market development across Cyprus.

Summary of Cyprus Real Estate Market Report

To start this Cyprus real estate market report, let us provide you with a summary of the findings based on the official data from the Cypriot government and the Cypriot central bank.

Foreign Property Buyers in Cyprus

According to data by the Cypriot Department of Lands and Surveys, a peak of up to 40% of all property purchases have been made by foreigners in Paphos in 2020/21. While this was a rising trend in all districts except Nicosia up until late 2020, the future share of foreign property buyers in Cyprus needs to be seen due to the latest global developments (Covid and its aftermath, end of the Cyprus CBI program, inflation, Ukraine invasion, etc.).

Most foreign buyers purchase properties in Paphos and Limassol in recent years, while the least foreign buyers purchase homes in Nicosia. Transactions are often made to gain permanent residence and/or as an investment through long-term rentals of these homes.

On the other hand, this means that at least 60% of property purchases (in Paphos), but generally closer to 90% on average, are made by Cypriots, meaning the domestic market for own use, buy-to-let properties, office spaces, and land is stable. Most domestic property transactions are made in Nicosia, the country’s capital and work hub.

In the last two years, the number of foreign buyers was by far highest in Paphos (40%-41%), followed by Larnaca (20%-21%), Limassol (18%-19%), Famagusta (14-19%), and Nicosia (8%). Paphos is most popular among British retirees, and Nicosia is least popular among foreigners.

The overall surge of foreign home buyers in 2020 can be attributed to (1) the discontinuation of the citizenship through investment program (real estate route) at the end of that year, and (2) Brexit in early 2020 with a grace period until the end of 2020, where investors took advantage of the closing opportunities.

As property transfers typically are lengthy processes, some transfers that were started in 2020 were closed, and therefore documented, in 2021. That year, the Cypriot government further incentivized the Cypriot residency by investment program (RBI) through real estate investment. This makes it likely that foreign property buyers continue to invest in this program.

Residential Property Price Index Development

According to the Residential Property Price Index (RPPI), published by the Central Bank of Cyprus, prices for houses are stable at a relatively low rate, which makes property purchases attractive as an investment. On the other hand, price points for apartments are rising, particularly in Limassol and Nicosia.

The RPPI bottomed out in 2016 and has been gradually, slowly increasing since. At the moment property prices are 20% lower compared to the year 2010. Limassol is at about 90%, Paphos at 80%, and Larnaca, Famagusta, and Nicosia are at around 70% compared to the property prices in 2010. The House price index is rising only very slowly, while the price index of apartments is rising more strongly, particularly in Limassol and Larnaca.

While houses have similar price points across all districts in Cyprus, the price points for apartments vary significantly and are proportionally higher than house prices.

In terms of affordability within the Cypriot districts, Larnaca is still on the lower end with a positive price development. The Larnaca Marina project, which has now started in 2022, will likely contribute highly to the overall growth.

In comparison, Limassol is relatively expensive but had continuous growth. Paphos, Famagusta, and Nicosia see a flattening development of moderate prices.

Development of Property Numbers, Values, and Average Investments

Overall, the lowest number of property transactions occurs in Famagusta while the highest number of transactions occur in Nicosia and Limassol. In particular, Larnaca and Nicosia experienced a steep rise of property transfers in 2020/21, whereas Paphos and Limassol saw slower growth rates.

On the other hand, in terms of total property transfer value, Paphos has fallen steeply and Famagusta is slowly declining – including seasonal investments and hotels. Larnaca and Limassol have been developing flat and stable. While the property transfer values in Nicosia fell between 2018 and 2020, they completely recovered in 2021 with a strong increase.

Overall, there is a declining trend in average investment value per property. Between 2016 and 2019 the number of property transactions increased while the total transaction value declined. Therefore, less expensive properties (or smaller properties) are bought more.

Outlook

In 2022, the development of the overall real estate transactions remains to be seen in the face of Covid, the invasion of Ukraine, inflation, and higher interests on mortgages. So far, the development is positive.

In the first five months of 2022, a total of 5,090 real estate transactions were made. That’s a 42% increase from the same period the previous year when Covid restrictions were still very strict.

Looking at the demographic development in Cyprus, it is interesting to note that the country’s population continues to grow (albeit slower) – unlike many other European countries. For example, in Germany, population growth has reached zero in 2020.

For Cyprus, the continuous population growth is good news as it contributes to the positive development of the property market, together with business- and lifestyle-related immigration.

A continuous rise of foreign property buyers in 2022 is expected due to the increasing number of foreign HNWIs seeking opportunities abroad due to the situation in their home countries (e.g. Ukraine, Russia, China) as well as swift investors trying to get ahead/leverage the global recession.

Cyprus Real Estate Market Report – Latest Developments

To start this Cyprus real estate market report, let’s take a look at the latest real estate-related developments. Until today, the Cypriot real estate and construction sector remain an economic driver on the island.

Economic Impact of Real Estate & Construction Sector

In fact, the real estate and construction sector contributed 16% to the country’s Gross Value Added (GVA) in 2021. The apartment market (especially between 100,000€ and 300,000€) together with land transactions are key drivers for the segment’s growth.

In particular, investors seize the opportunity of the previously low interest and strong rental market to purchase rental properties and vacation homes. With gradually increasing key interest rates this is now slowly changing. Buy-to-let real estate is increasingly popular in Cyprus due to its attractive return on investment of 5%-7%.

In terms of districts, Nicosia contributes to the real estate sector growth in terms of transaction volume (domestic residential demand) while Limassol contributes via the total transaction value.

The key drivers for the domestic housing market are disposable household income and mortgage interest rates, while global economic and political developments impact the foreign housing market in Cyprus.

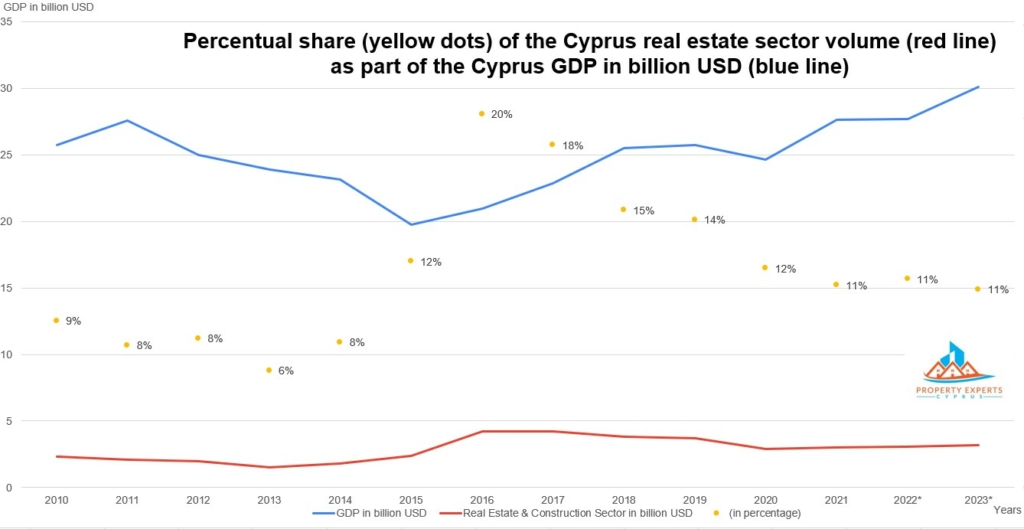

Correlation between Cyprus GDP and Real Estate Sector Volume

The Cypriot real estate and construction sector contributed on average 12% (2010-2021) to the country’s GDP, mainly driven by the Golden Passport program through foreign real estate investments. As this program has been discontinued in October 2020, the exact relevance of the real estate industry in Cyprus to the country’s economy remains to be seen.

However, the projection for the near future by industry experts sees a solid growth of the Cypriot GDP and real estate sector.

This chart shows the percentage share (yellow dots) of the Cypriot real estate sector volume (red line) compared to the Cyprus GDP in billion USD (blue line).

Cyprus Golden Passport Discontinued

The halt of the Citizenship by Investment Program (Golden Passport) in late 2020 also put an end to overpriced properties and many developers offer less expensive apartment and housing options.

While this is generally a positive effect for home buyers and renters, it forced property owners and developers to tap into new local target audiences and markets.

Nonetheless, to date around half of the properties bought in Cyprus every year are acquired by foreigners to obtain a Golden Visa (residency) as well as to leverage tax and business advantages. This trend persists despite the Golden Passport (citizenship) discontinuation and Covid disruptions.

Finally, these latest developments haven’t stopped property developers from slowing down. Many of them have successfully shifted their markets, resulting in a 17% increase of new building permits in 2021 at an overall lower volume, indicating smaller-scale projects to offer more affordable housing options for their local and international customers.

Cyprus Golden Visa Program Still Strong

Fueled by recent economic and political events, the Cypriot residency by investment program is more popular than ever. Global HNWIs, investors, retirees, and their family members benefit from a fast and efficient EU residency through real estate investment. It allows the holder to live, do business, and study in Cyprus.

With the 2021 updates to the Cyprus Golden Visa program, residency through real estate investment in Cyprus has become even more attractive.

- Since March 2021, a bank deposit and Cypriot bank account are no longer required for the residency program.

- The real estate investment can now also be made with second-hand commercial properties, in addition to new properties from developers. The restriction of a maximum of two properties for investment has been lifted for second-hand commercial properties. However, residential and commercial investments cannot be combined.

The Cypriot RBI starts with real estate property investment from 300,000 EUR (~363,000 USD) plus lawyer costs, stamp duty, and VAT. Discover attractive apartments and houses to buy in Cyprus here.

Covid Effects

The positive impacts of the Cypriot housing and construction industry remain strong despite the travel and investment disruptions caused by the Covid-pandemic in 2020 when the Cyprus GDP decreased by 4%.

The Covid-pandemic caused a shift in the target audience of property owners and developers in Cyprus: renting or selling apartments and houses to locals at a lower budget is now a more profitable approach then high-end rentals and sales to foreign HNWI (who bought properties for the citizenship route in the past).

Before this shift, the Cyprus real estate market crashed for a brief period, caused by a global halt of travel and investments, the discontinued CIP program, and Covid-induced increase in costs of construction materials.

The Cypriot real estate market is again under pressure in 2022, caused by global developments, including the invasion of Ukraine, worldwide inflation, as well as Covid-caused supply chain disruptions.

To combat the effects of the global pandemic, the Cypriot Government implemented an interest subsidy scheme to help the local economy recover. As a result, new mortgage loans worth 1.3 billion Euros were taken out in 2021.

Affordable Real Estate in Cyprus

Overall, while rent is comparatively high, buying and owning real estate in Cyprus is very affordable compared to the rest of Europe/the EU while the rental ROI is reasonable and gradually increasing. Take a look at this extensive article and comparison of global property prices and real estate ROIs.

This is the latest Numbeo data for the overall country rank and the price to income ratio, as well as the price per square meter to buy an apartment in the city center and the price per square meter to buy an apartment outside the city center.

The price to income ratio refers to apartment purchase affordability (lower is better). It sets median apartment prices in relation to median familial disposable income.

| Country | Price to Income Ratio | Price/Sqm to buy an apt. in city center | Price/Sqm to buy an apt. outside city center | Average Real Estate ROI* |

| South Africa | 3.07 | 1,015$ | 763$ | 9% |

| USA | 3.96 | 4,520$ | 2,162$ | 7% |

| Cyprus | 6.4 | 2,079$ | 1,480$ | 7% |

| Italy | 8.61 | 4,191$ | 2,414$ | 3% |

| Spain | 8.78 | 3,221$ | 1,983$ | 5% |

| UK | 8.86 | 5,059$ | 3,861$ | 4% |

| Germany | 8.93 | 7,221$ | 5,142$ | 3% |

| France | 9.94 | 6,934$ | 4,795$ | 2% |

| Greece | 10.12 | 2,085$ | 1,758$ | 4% |

| Portugal | 12.25 | 3,080$ | 2,140$ | 5% |

| Malta | 13.11 | 3,673$ | 2,651$ | 5% |

| Israel | 13.51 | 7,534$ | 6,111$ | 3% |

* ROI = rental price per year (1-bedroom apartment in the city center) / purchase price (for a 60sqm apartment in the city center based on theNumbeo cost of living overview per country)

The Specialities of Each Cypriot District

The real estate and construction sector in Cyprus saw a boost in 2015/16 but has since plateaued. In 2021, the total transaction volume reached 3.8 billion Euros (~4 billion USD) with transactions of around 19100 properties. Due to the latest global developments, the development trend of the Cypriot real estate sector remains open.

The key drivers continue to be the districts of Nicosia and Limassol. This trend is expected to continue, albeit slowly flattening. Larnaca district with its high-value development projects is likely to be a new driver for the real estate sector in Cyprus.

Generally, each Cypriot district has its own target audience for the real estate market.

- Nicosia: capital city, strong rental, and office segment (local market)

- Limassol: luxury rental properties, new development projects like the Limassol Marina, skyscrapers, and casinos, favored by Russians

- Paphos: beautiful beaches, high-end properties, favored by British holidaymakers and retirees

- Larnaca: new development projects like the Larnaca Marina, large Israeli community of investors

- Famagusta: main holiday region with beautiful Blue Flag beaches, new developments projects like the Agia Napa Marina

Based on the data analyzed, property investors who buy to let do so for long-term rental properties rather than short-term holiday rental properties (e.g. Famagusta). The reason is often that the investors purchased properties to gain permanent residency, but don’t live here themselves.

Therefore, long-term rental properties are more common than short-term holiday rentals for investment, which typically require pricy property managers and come with additional liabilities like wear and tear, damages, and so on.

Now, let’s dive deeper into the Cyprus real estate market report.

Cyprus Real Estate Market Report – Buyer Profile

Based on the official data of the Cypriot Ministry of Interior, Department of Lands and Surveys (DLS), we have created a real estate buyer profile per district for the last six years.

We’re comparing foreign property buyers and local Cypriot buyers (Foreign Buyers Sales and Contracts of Sales) as well as the total number of property transactions (transfers of sale) and their value (accepted amount).

Nicosia

The foreign property buyer share is low overall in Nicosia.

| Year | Total Transfers | Foreign Buyers | Domestic Buyers | Total Property Value in EUR (Sales Amount) |

| 2016 | 3,563 | 165 (5%) | 3,398 (95%) | 992,107,098€ |

| 2017 | 3,767 | 152 (4%) | 3,615 (96%) | 946,033,098€ |

| 2018 | 4,215 | 28 (1%) | 4,187 (99%) | 965,213,443€ |

| 2019 | 4,332 | 73 (2%) | 4,259 (98%) | 910,306,516€ |

| 2020 | 3,990 | 299 (8%) | 3,691 (92%) | 834,936,932€ |

| 2021 | 5,530 | 474 (8%) | 5,056 (92%) | 955,336,767€ |

The total number of foreign buyers is just slowly rising. The number of property transactions and correspondingly the total property value back to pre-Covid with strong demand in 2021.

Famagusta

Overall, the least amount of properties are transferred in Famagusta.

| Year | Total Transfers | Foreign Buyers | Domestic Buyers | Total Property Value in EUR (Sales Amount) |

| 2016 | 790 | 43 (5%) | 747 (95%) | 204,093,394€ |

| 2017 | 872 | 44 (5%) | 828 (95%) | 342,682,685€ |

| 2018 | 987 | 48 (5%) | 939 (95%) | 255,217,248€ |

| 2019 | 895 | 50 (6%) | 845 (94%) | 190,976,345€ |

| 2020 | 839 | 161 (19%) | 678 (81%) | 155,899,378€ |

| 2021 | 1,010 | 147 (14%) | 863 (86%) | 179,560,850€ |

The total number of foreign buyers rapidly started rising in 2020. The number of property transactions is low but relatively stable, however, the property transaction values have been decreasing since 2018, albeit not as steeply as in Paphos.

Larnaca

Like in Famagusta, the total number of foreign buyers rapidly started rising in Larnaca in 2020.

| Year | Total Transfers | Foreign Buyers | Domestic Buyers | Total Property Value in EUR (Sales Amount) |

| 2016 | 2,338 | 174 (7%) | 2,164 (93%) | 503,595,518€ |

| 2017 | 2,458 | 163 (7%) | 2,295 (93%) | 493,591,883€ |

| 2018 | 2,630 | 54 (2%) | 2,576 (98%) | 437,325,144€ |

| 2019 | 2,875 | 149 (5%) | 2,726 (95%) | 474,093,414€ |

| 2020 | 2,237 | 467 (21%) | 1,770 (79%) | 363,446,139€ |

| 2021 | 2,694 | 552 (20%) | 2,142 (80%) | 450,361,068€ |

The number of property transactions was slowly rising and took a dip in 2020. It seems the market is now recovering. Alongside Nicosia, Larnaca is the only district that continued to show rising property transfer numbers (except for Covid-caused dip in 2020).

Limassol

As in the previous districts, the total number of foreign buyers rapidly started rising in 2020.

| Year | Total Transfers | Foreign Buyers | Domestic Buyers | Total Property Value in EUR (Sales Amount) |

| 2016 | 3,792 | 281 (7%) | 3,511 (93%) | 1,258,193,086€ |

| 2017 | 4,358 | 271 (6%) | 4,087 (94%) | 1,461,095,686€ |

| 2018 | 4,280 | 193 (5%) | 4,087 (95%) | 1,251,334,627€ |

| 2019 | 4,262 | 203 (5%) | 4,059 (95%) | 1,273,998,747€ |

| 2020 | 3,370 | 595 (18%) | 2,775 (82%) | 900,993,520€ |

| 2021 | 4,409 | 819 (19%) | 3,590 (81%) | 1,096,801,468€ |

The number of property transactions is relatively stable. The 2020-dip caused by Covid and the end of the CBI program was most visible in Limassol.

Paphos

While the number of total property transfers are continuously declining, Paphos has experienced the steepest decline in total property value over the last six years.

On the other hand, Paphos has by far the highest share of foreign buyers, which rapidly started rising in 2020 – just like in the other districts.

Therefore, it can be concluded that Paphos district feels the impact of the end of the CBI program the strongest. Likely, most foreign investors are British who bought real estate “regularly” while Britain was still part of the EU, and now buy property through the Golden Visa route to obtain residency in Cyprus.

| Year | Total Transfers | Foreign Buyers | Domestic Buyers | Total Property Value in EUR (Sales Amount) |

| 2016 | 3,060 | 295 (10%) | 2,765 (90%) | 1,023,345,414€ |

| 2017 | 2,757 | 226 (8%) | 2,531 (92%) | 802,325,408€ |

| 2018 | 3,087 | 106 (3%) | 2,981 (93%) | 703,939,912€ |

| 2019 | 3,081 | 437 (14%) | 2,644 (86%) | 704,426,209€ |

| 2020 | 2,272 | 910 (40%) | 1,362 (60%) | 479,300,691€ |

| 2021 | 2,592 | 1,065 (41%) | 1,527 (59%) | 509,298,538€ |

Housing Index Development – Cyprus Real Estate Market Report

Next, here’s a detailed analysis of the Cyprus housing market development based on the data of the Central Bank of Cyprus.

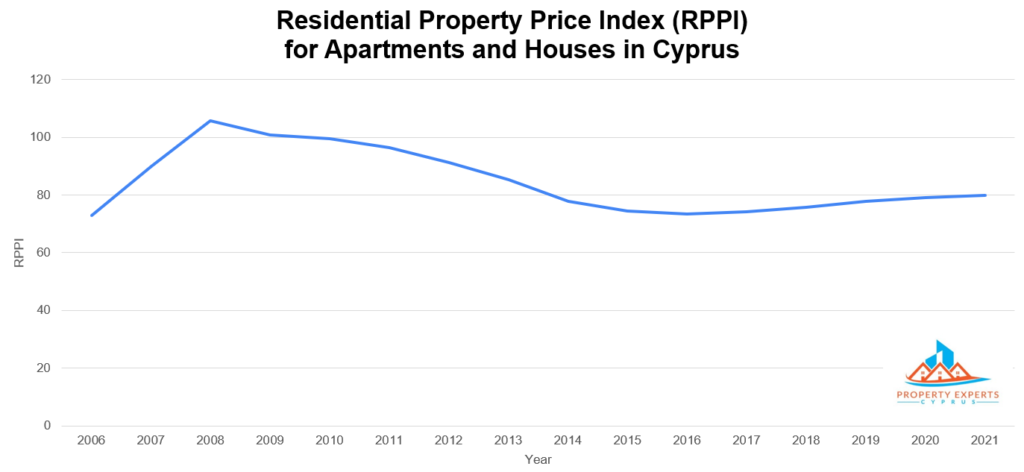

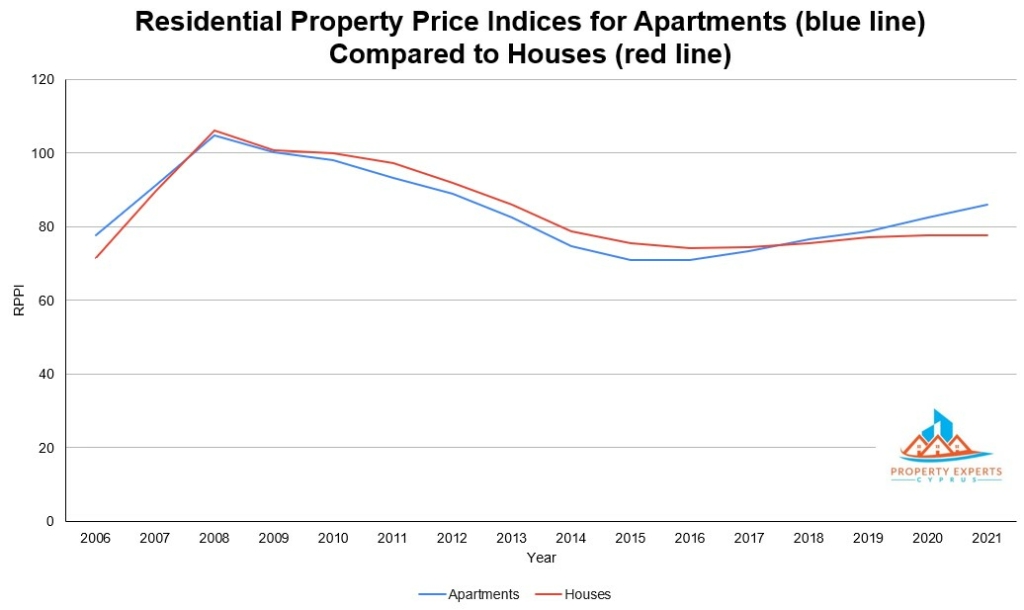

Residential Property Price Index (RPPI)

The RPPI is calculated on the basis of market valuations of real estate prices in combination with best-practice statistical methodology. This data by the Cypriot central bank is representative of the Cyprus property market, covering all districts. It refers to residential properties, both houses, and apartments. The base period for all indices is the first quarter of 2010 with a value of “100”.

It shows the relative price development of apartments and houses in Cyprus, which have now stabilized at a relatively low index rate of around 80, so 20% less expensive compared to the year 2010. This is interesting as property prices in the rest of Europe have continued to rise.

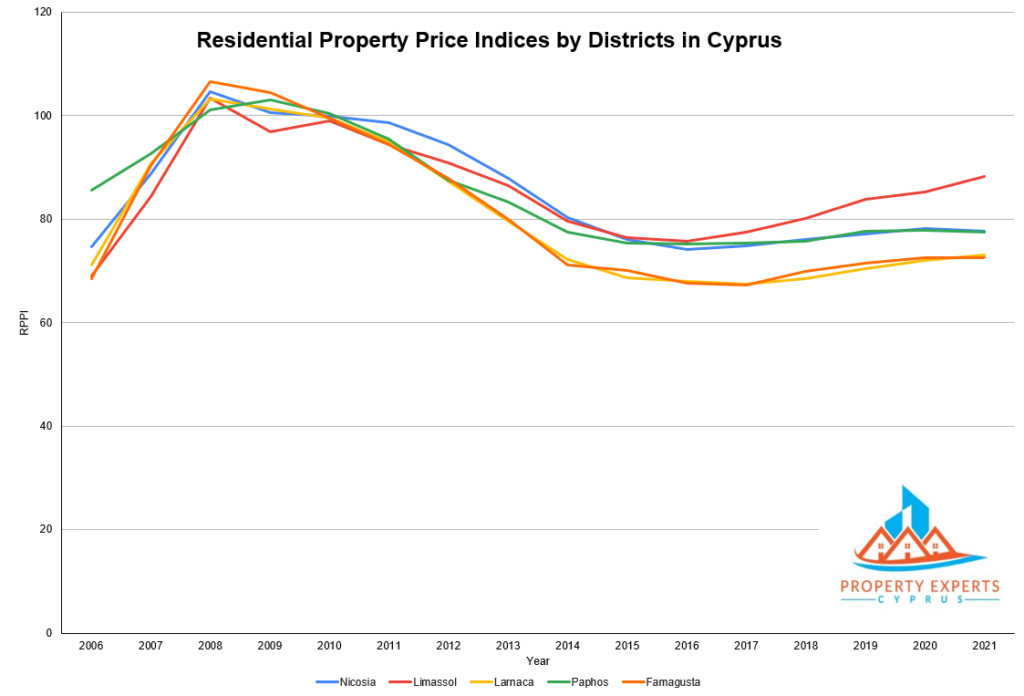

Residential Property Price Indices by Districts

The residential apartment and house prices develop similarly across all districts. Homes are most affordable in Famagusta and Larnaca, followed by Paphos and Nicosia. Homes are most expensive in Limassol.

Residential Property Price Indices by Apartments and Houses

Likewise, the price points of apartments and houses in Cyprus develop similarly. However, since 2018, apartments are more expensive compared to houses.

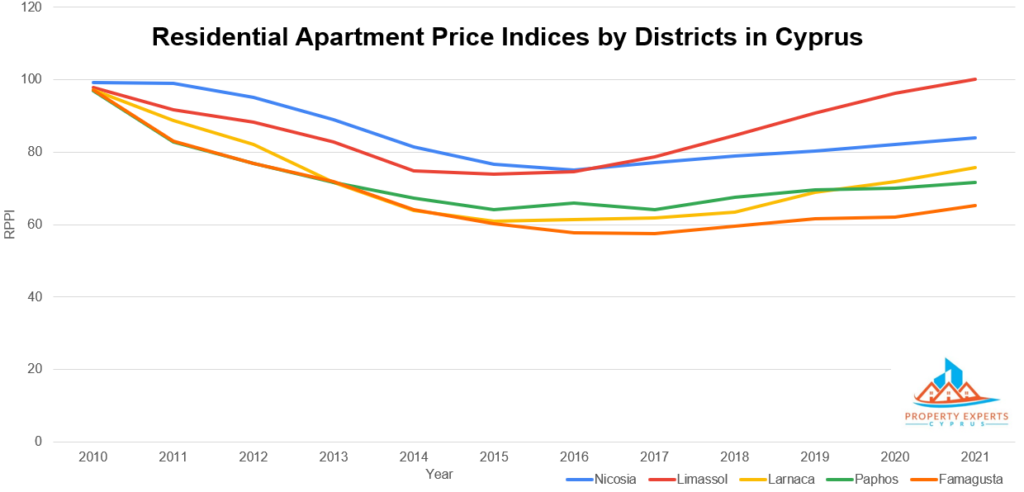

Residential Apartment Price Indices by District

Apartments are most affordable in Famagusta, followed by Paphos and Larnaca. The most expensive apartments in Cyprus are located in Limassol and Nicosia, where the main job markets of the island are.

Price points for apartments on the island have a relatively wide range. Apartment prices in Limassol and Larnaca are steeply rising while prices in Famagusta are moderately rising. The prices for apartments in Paphos and Nicosia are plateauing. In terms of apartment prices, Larnaca surpassed Famagusta in 2015 and Paphos in 2019.

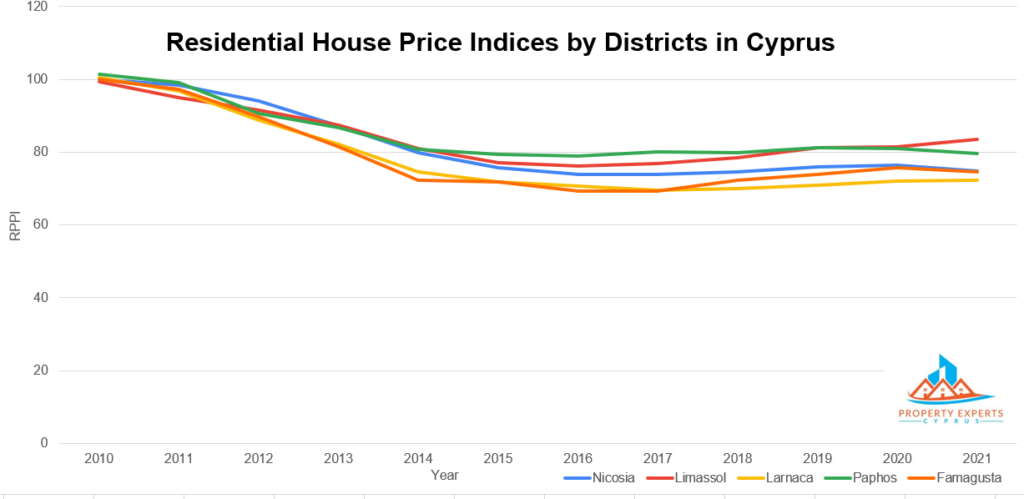

Residential House Price Indices by District

Unlike apartments, price points for houses in Cyprus are rather homogenous. With small differences, Larnaca, Famagusta, and Nicosia have slightly more affordable houses compared to Paphos and Limassol.

Analysis of the Cyprus Real Estate Market Report

According to the data from the Cypriot Central bank, residential property prices indicate that Cypriot buyers invest more in smaller or less expensive homes in all districts, especially from 2020/21.

Since Q2/2022, an increasing number of foreigners (in particular Israelis, Russians, Chinese) invest in buy-to-let apartments and houses (long-term rentals) as prices are very affordable compared to their home countries.

At the same time, an increasing number of Ukrainians and Russians are relocating to Cyprus for work respectively, setting up their business and buying or renting homes for themselves and their families.

Besides, the trend among global businesses to relocate their headquarters (“headquartering”) to Cyprus due to the country’s favorable tax regulations and strong workforce, leads to an increased demand for office spaces and homes for the international staff – especially in Nicosia and Limassol, which are the main job markets.

This brings us to the end of this extensive Cyprus real estate market report.

Cyprus Real Estate Market Report – The Takeaway

This Cyprus real estate market report reveals that while rent is comparatively high, buying properties in Cyprus is still very affordable, especially compared to other destinations in Central and Southern Europe. In the past, foreign real estate investments were boosted by the Cyprus Golden Passport (citizenship) program, which was discontinued in late 2020.

Nonetheless, the “Jewel of the Mediterranean” remains attractive overall among foreign HNWIs, investors, and retirees, and the Golden Visa (residency) program continues with popularity.

Properties are purchased up to 40% by foreigners (mainly in Paphos), typically by Russians, Chinese, and Middle Eastern investors as well as British and German retirees. The majority of property purchases continue to be made by local Cypriots – in particular in Nicosia. With the invasion of the Ukraine and consequent sanctions against Russian investors, their investment trends in Cyprus remain to be seen.

Since Q2/2022 foreigners are increasingly investing in buy-to-let properties (long-term) – in particular, in Limassol and Paphos – due to the comparatively affordable prices and low taxes. Besides, the rental market is booming, in particular, domestic residential properties and offices (due to “headquartering”).

However, the Cypriot real estate market is again under pressure in 2022, due to global developments, like the invasion of Ukraine, worldwide inflation, and supply chain disruptions caused by Covid. Therefore, the short- and mid-term developments of the Cypriot real estate market remain under pressure.

Are you keen to lift the potential of the attractive real estate investment sector in Cyprus? Contact the specialists at Property Experts Cyprus to get started with your free consultation.

Disclaimer: The information in this Cyprus real estate market report has been researched to the best of our knowledge and is dated Q3/2022. Investment tactics depend on your specific personal situation and knowledge, which is why this article may NOT be construed as investment or financial advice.